Cleantech.com – Green H2 for Global Decarbonization

By Louis Brasington, in Cleantech.com

December 13, 2018

There are over 60 million tons of hydrogen produced annually, worth almost $100 billion dollars. Today, 80% of the hydrogen we produce is for three main industries: refineries, ammonia production or metal processing.

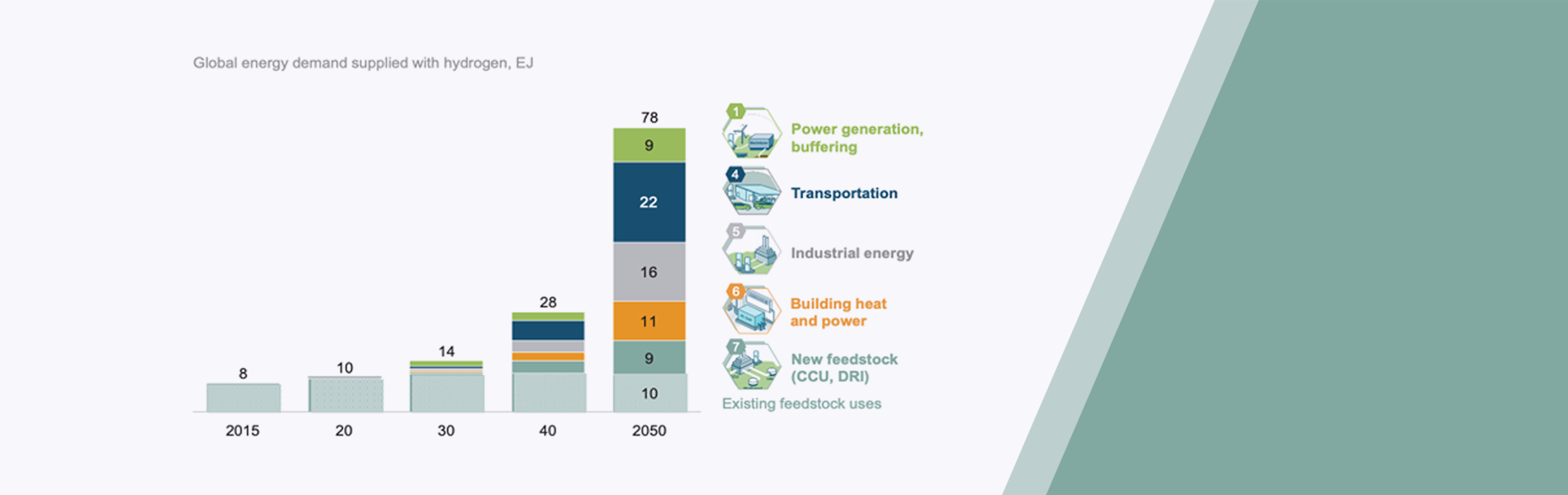

Hydrogen also has the potential to be used as fuel for power and transportation. It generates zero emissions at point of use and can be produced from low-carbon electricity or from carbon-abated fossil fuels. The annual demand for hydrogen could increase tenfold by 2050 – from 8 EJ in 2015 to almost 80 EJ in 2050 (see figure 1 courtesy of the Hydrogen Council).

Hydrogen and the Auto Industry

Hyundai Motor and Yield Capital plan to raise $100 million for a Hydrogen Energy Fund, predicting that numerous new hydrogen startups will come about over the coming years. This summer, France announced $117 million of funds dedicated to deployment of hydrogen in industry, mobility and energy, recognizing that “H2 can become one of the pillars of a carbon-neutral energy model”. Japan also has one of the most progressive plans for the use of Hydrogen for fuel-cell vehicles (FCEV), given their strategy of aiming to build out the Hydrogen High Way with hundreds of hydrogen fueling station. They plan to halve the cost of building a hydrogen fueling station by 2020

Green Hydrogen Production

To achieve net-zero CO2 emission targets, global hydrogen production needs to rise from about 60 million tons a year to 500-700 million tons by mid-century, without considering rapid uptake of Fuel cell electric vehicles (FCEV). Coupling hydrogen production with renewables is a viable path to achieve this. In fact, 95% of today’s global production of hydrogen is from carbon-based CO2 emitting methods: natural gas steam methane reforming (SMR) and coal gasification.

The Economic Case for Production

Producing low-carbon hydrogen cost-effectively remains one of the key barriers for wide-scale hydrogen system deployment. Outside of carbon-based generation, water electrolysis remains the current frontrunner, despite still only accounting for around 4% of global hydrogen production. With the increased capacity of renewables on the grid, low-carbon electricity may make economic sense, in some markets, to transform hydrogen to power. Two frontrunner electrolysis technologies exist: Alkaline and PEM (proton exchange membrane) electrolysis. Alkaline technology is mature and lower-cost, having been used since the 1920s to produce hydrogen centrally in large quantities. PEM technology is newer and characterized by higher efficiencies, a smaller footprint and a better capacity to operate under flexible, decentralized operations.

PEM for Green Production

PEM is now approaching technical maturity and economies of scale for operation on a megawatt basis. Commercial deployment has started in several regions of the world (Japan, California and Europe). One of the biggest PEM projects underway is H2FUTURE in Linz, Austria which is due for completion early 2019. Green hydrogen will be produced from a 6 MW PEM electrolysis system, developed by Siemens, with the goal of achieving 80% efficiency in converting electricity into hydrogen. The hydrogen produced at Voestalpine’s steel manufacturing site, will be used for demand side management, helping to compensate for power fluctuations in an increasingly volatile power supply, enabling higher shares of wind and solar energy on the grid. It will also be fed directly into the various stage of steel production, replacing carbon-based feedstock for heating, power and and feedstock requirements. This industrial application could be key for realizing full decarbonization of the steel industry, which today accounts for 4% of global emissions.

Renewable Power-to-Hydrogen – The Bigger Opportunity

The H2FUTURE project touches on the wider potential for electrolysis’ when technology is developed for point-of-use application. Built-in storage capacity of downstream sectors can be used as a buffer to adjust hydrogen production – and hence electricity consumption in real-time – depending on the needs of the power system, absorb variable renewable energy (VRE) possibly over long periods and allow for seasonal storage. Ultimately, this creates a market opportunity for onsite hydrogen that cannot be served from battery technology. Figure 3 demonstrates how integration of electrolysis combined with VRE can facilitate coupling between electricity and buildings, transport and industry.

Solid-Oxide Electrolysis (SOEC)

SOEC, is a newer electrolysis technology that works at high temperatures typically between 500 and 850 °, and has the potential of superior efficiencies than ALK and PEM. Sunfire, is a SOEC startup substantially down the commercialization path, and a four-time GCT100 company. The company is developing solutions to produce renewable synthetic fuels, and is starting to deploy energy service solutions for different industry applications. The GrinHy project is integrating Sunfire’s modular electrolyzers into industrial processes at a steelworks, to be stackable up to the megawatt scale.

The technology’s reversible, dual-mode system can be used either as an electrolyzer for green hydrogen production at 80% electrical efficiency, or as a fuel cell, where the system creates heat which can be fed back into the steelworks and the electricity used for grid stabilization.

Emerging New Technology

Some alternative electrolysis technologies that address existing challenges with current methods are coming onto the market. For example, Anion Exchange Membrane (AEM) electrolysis combines benefits of both Alkaline and PEM, while simultaneously overcoming drawbacks. AEM is low-cost, energy efficient, can use rain or tap water, and is stackable, meaning it can be easily applied at any scale. Founded last year, Enapter is commercializing an AEM electrolyzer technology that has been in development for seven years. The startup is also one of the first to develop a priority energy management system, enabling integration of modular hydrogen systems into the grid.

Cost-efficient, scalable distributed resource management systems are vital in today’s energy market, helping to capture the highest value from distributed assets as they integrate with current networks and markets. Today, not many players have tried to create connected energy management systems. If players can accelerate the rate at which low-cost, efficient hydrogen system can be part of the DER transition, and hydrogen integrated Smart grid systems could can come in play as early as 2020. Enapter wants to run commercial-scale mass-production of their EMS in combination with AEM systems from next year across the globe.

The Business Case for Green Hydrogen

The business case for hydrogen using VRE in off-grid settings remains challenging. Rapid scaling up is now needed to achieve the necessary cost reductions and ensure the economic viability of hydrogen as a long-term enabler of the energy transition.

Progressive deployment requires ramping up of a hydrogen supply chain, including additional capacity for distribution. Today the cost and safety of hydrogen transport remains a key barrier. On-site generation solves for point-of-use applications, but ultimately hydrogen needs a means to be transported at ease to for its other markets. The UK’s H21 Project is a promising project sets out a strategy to rollout hydrogen conversion across the North of the UK, which ultimately achieves deep decarbonization of the whole of the UK with three steps. First just heat, then heat and power and finally removal of 83.5% of the CO2 required to be removed from the country’s emissions to meet its 2050 target. The project will demand sustained commitments from public and private stakeholders, with the total CAPEX cost of system conversion for H21 NOE has been assessed to be around $28.6 billion, with a per annum OPEX of $1.2 billion.

The report foresees a future where hydrogen could be used to balance global renewable energy requirements: “Countries with vast renewable excess, for example Australia, a continent with 24 million people, could trade green energy in the form of hydrogen shipped as ammonia with countries with renewable shortages, for example the UK with 66 million people.”

May of the leading players including Air Liquide are starting to deploy large-scale hydrogen infrastructure, driven by the need to meet the fuel demands of Fuel Cell Electric Vehicles (FCEVs). New players such as H2GO Power are developing solid-state hydrogen storage, directing addressing safety and efficiency loss concerns with compression and liquidation, and are looking to finish a pilot project next summer. Australia’s Project H2GO, announced in October, is also using renewables to produce hydrogen for long-term energy storage in the Sydney Gas network.

Hydrogen’s Challenge:

Widespread uptake of hydrogen requires large CAPEX risks for financiers of structural development. Costs need to continue to reduce for megawatt scale electrolysis if green hydrogen can replace carbon-based hydrogen for industrial feedstock applications. Focused, predictable energy policy is needed from all participating governments in order to provide the long-term stability needed for large investments into hydrogen. Local community acceptance barriers exist around establishing infrastructure and overcoming the perception of safety.